The wheel of fortune turns.

With the release of the half-year data for power batteries, the situation has become even clearer.

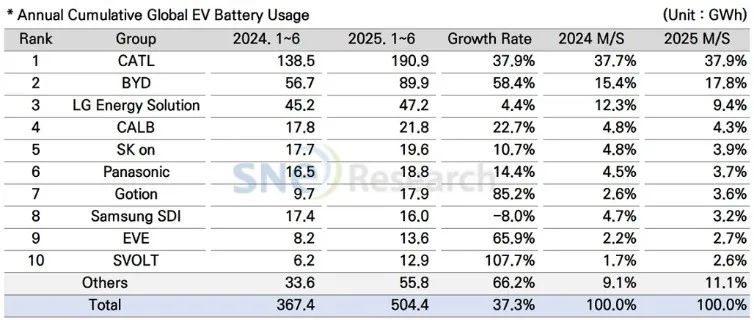

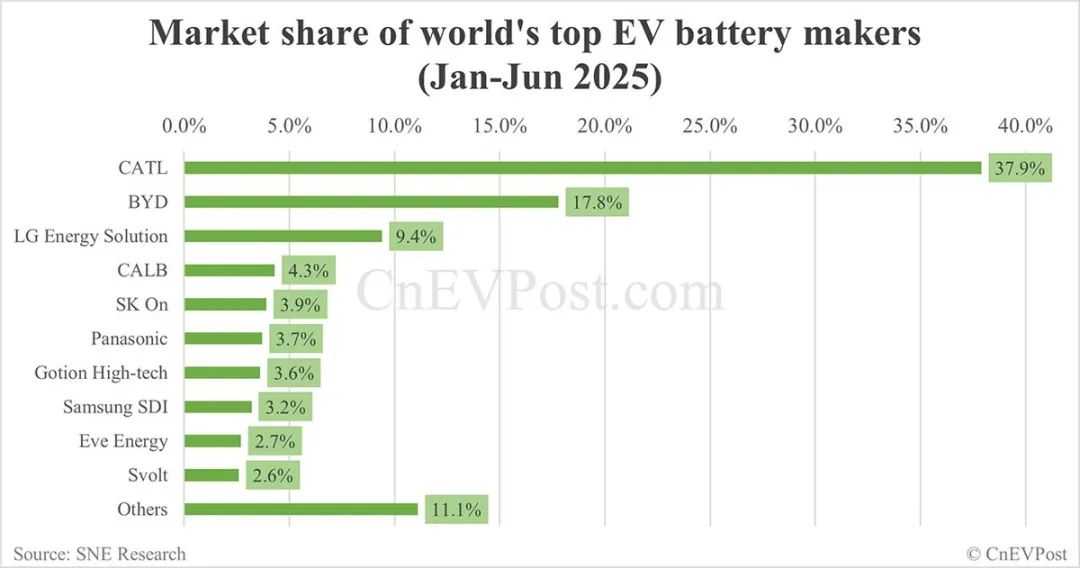

According to the latest data from South Korean research firm SNE Research, global EV (EV, PHEV, HEV) battery installations in H1 2025 reached 504.4 GWh, up 37.3% YoY. Meanwhile, the once dominant Japan and South Korea battery producers saw their market share further decline.

LG Energy Solution, SK On, Samsung SDI, and Panasonic together had a total installation of 101.6 GWh, accounting for a combined market share of 20.1%, down 6.1% YoY. In other words, they did not outperform CATL alone (190.9 GWh). At the same time, they could not escape the "80/20 rule".

Chinese companies occupied six spots in the top 10, with a combined installation of 347 GWh, reaching a market share of 68.8%, up 4% YoY, continuing to surge ahead. As the center of the global power battery industry shifts, the LFP route is still "marching from victory to victory".

01 The Three Korean Giants, Outmatched by BYD

In this list released by SNE, not only did the three Korean battery giants LG Energy Solution, SK On, and Samsung SDI fail to outperform CATL, but they also fell short against the second-ranked BYD. BYD's installations reached 89.9 GWh, raising its global market share to 17.8%.

It must be said that the momentum of Chinese battery companies caused the market share of three Korean giants to fall 5.4% YoY.

Among the Korean giants, LG Energy Solution experienced the most significant drop in market share. Although LG Energy Solution still ranked third with 47.2 GWh in installations, it grew only 4.4% YoY, with its market share falling from 12.3% in 2024 to 9.4% this year.

According to SNE's analysis, the main reason is that LG Energy Solution's batteries are primarily used by car makers such as Tesla, Chevrolet, Kia, and Volkswagen. For Tesla, "due to the decline in sales of models equipped with LG Energy Solution batteries, Tesla's usage of its batteries decreased by 41.1%."

Of course, thanks to the strong global sales of Kia EV3 and the expanded sales of Equinox, Blazer, and Silverado EV, which are based on the Ultium platform, in the North American market, LG Energy Solution managed to save some face.

The root of LG Energy Solution's predicament lies in its wavering technological path. Hesitation between ternary lithium batteries and LFP batteries led to the loss of Tesla's 4680 battery orders. Additionally, its cost control weaknesses were evident; according to media reports, the unit manufacturing cost at its Nanjing factory was 18% higher than that of CATL, leading to a gradual loss of competitiveness in the low and mid-end markets.

Among these three, Samsung SDI fared the worst. It was the only company among the top 10 to experience negative growth, with its market share dropping from 4.7% in 2024 to 3.2% this year due to an overemphasis on solid-state batteries. Moreover, according to predictions by Morningstar analysts, Samsung SDI is expected to incur an operating loss of 398 billion won (approximately 2.06 billion yuan) in 2025.

Another company, SK On, ranked fifth with 19.6Gwh of installations, up 10.7% YoY, but its market share fell from 4.8% in 2024 to 3.9% this year. The main reason for the decline was the weakening demand for its batteries in the European and North American markets.

Interestingly, since 2021, SK On has been incurring losses. In 2024 alone, the loss amounted to 1.127 trillion won (approximately 1.797 billion yuan). Furthermore, the projected losses for 2025 are expected to continue growing. For instance, Nomura Orient International Securities forecasts that SK On's operating profit will suffer a loss of $340 million (approximately 2.44 billion yuan) this year.

As the saying goes, "fortune turns," and it took just a few years for the three Korean giants to fall from their dominant position in the global market to their current state.

In fact, as early as Q1 2020, LG Chem (the predecessor of LG Energy Solution) alone had a global power battery market share of 27.1%. The combined market share of Samsung SDI and SK On also reached 21.1%, with the "big three" accounting for nearly 50% of the global market share. Compared to the peak in 2020, the market share of the three Korean giants has fallen by about two-thirds over the past four years, which is quite lamentable.

Of course, behind this was the strong rise of Chinese battery companies and the mainstream adoption of LFP technology. From 2020 to now, the proportion of LFP batteries in the global power battery market surged from less than 20% at its lowest point in a single month to 78% in July 2025.

Therefore, the three Korean giants, who once abandoned the LFP route, were forced to catch up, including showcasing their LFP technology reserves at various exhibitions. However, they still lag far behind in mass production. For example, the yield rate of the LFP battery line at LG Energy Solution's Polish factory just exceeded 70%, which is a significant gap compared to the >90% or even over 95% yield rates of top-tier Chinese enterprises.

It is worth noting that while the three Korean companies are still hanging there, Panasonic is the only Japanese battery company to enter the top 10. With 18.8GWh of installations and a growth rate of 13.9%, Panasonic rose to sixth place, showing a relatively clear recovery trend. However, its market share dropped from 4.5% in 2024 to 3.7% this year.

Of course, its recovery benefited from a deep partnership with Tesla. After increasing the energy density of the 21700 battery to 290Wh/kg and reducing costs by 12%, Panasonic regained competitiveness in the Model 3/Y car models. However, the risk of relying on a single customer is also very evident.

02 The issue of technology confidentiality

For Japanese and South Korean battery companies, times are very tough now. Facing multiple operational pressures and market challenges, they can only initiate strategic business adjustments. For example, LG Energy Solution announced at the beginning of this year that it would cut its annual capital investment by 30%.

In April, LG Energy Solution declared its official withdrawal from a $8.45 billion (approximately 130 trillion Indonesian rupiah) battery industry integration investment project in Indonesia. However, shortly after, LG Energy Solution also announced an additional $1.7 billion investment into the HLI Green Power battery factory, scheduled to be operational by July 2024. This is a joint venture between LG Energy Solution and Hyundai Motor with a capacity of 10GWh.

Additionally, in April, LG announced that due to the continued sluggish global demand for electric vehicles (EVs), it would completely exit the EV charging piles business. Domestically, news of layoffs at LG's Nanjing plant occasionally surfaces.

Furthermore, in May, Panasonic CEO Yuki Kusumi stated that Panasonic would delay the establishment of its third battery plant in the US and focus on the commissioning of its second plant in Kansas. The planned annual capacity of this plant is 30GWh, with full production expected to start in 2026. However, due to the poor sales performance of Tesla car models, Panasonic is reassessing its production plans.

In the fierce international competition, a very important issue has been underscored: the confidentiality of China's LFP preparation technology.

As is well known, China holds technology advantage for LFP. According to the draft for soliciting opinions on the "Catalogue of Technologies Prohibited or Restricted from Export" released by China's Ministry of Commerce on January 2, 2025, "cathode material preparation technology" was explicitly listed under the restricted export category, including LFP, LMFP, and related raw material preparation technologies.

This adjustment aims to control the outflow of next-generation high-end LFP battery technology, consolidate domestic industrial advantages, and respond to international technological competition. The recent actions of the EU investigation team demanding sensitive information like battery formulas from Chinese automakers further highlight that the national level has recognized the importance of technological confidentiality.

Given the current situation, due to past technological missteps, Korean companies have also initiated a "talent poaching" mode in pursuit of rapid progress. For instance, in March this year, Jiemian News reported that LG Energy Solution would introduce the core team from Chinese battery company JEVE, with three batches totaling 200 people covering all key processes including R&D, production, and sales.

In 2024, Korean media also reported that LG Energy Solution was interested in JEVE's talent team and LFP technology, without any intention to purchase its factories or equipment.

Although the JEVE team is relatively small, its advantage lies in covering R&D, production, and sales, and it possesses complete R&D capabilities for prismatic LFP batteries. While its capabilities are not outstanding among Chinese battery companies, it is a timely help for Korean companies with significant weaknesses in their LFP business.

The primary task for the JEVE R&D team joining LG's Nanjing factory is to develop high-density, ultra-fast charging prismatic LFP batteries based on Lopal's high-compaction density LFP material. Additionally, LG Energy Solution has also approached Chinese equipment suppliers such as Lead Intelligent Equipment and Lyric, hoping to quickly enhance mass production capabilities.

Looking back, the key factor behind the comprehensive retreat of Korean battery companies was their weak LFP battery business. It is still very necessary for Chinese companies and relevant departments to take precautions against technology leaks.

It must be said that ternary lithium batteries once made Korean battery companies successful, but LFP batteries have made Chinese battery companies successful. Now, to avoid market elimination, Chinese battery companies need to continuously increase R&D and commercial validation of new technologies, including sodium-ion batteries, large cylindrical batteries, and solid-state batteries, to be prepared for any eventuality.

Overall, the data for H1 2025 also reflects, as industry insiders have summarized, that Chinese companies rapidly capture the market with a "fast technology iteration + cost reduction through scale" model. The competition focus of the power battery industry has shifted from a single technological barrier to an all-around efficiency contest centered on "technology conversion efficiency, cost control capability, and market response speed." Future competition remains full of uncertainties.

Please note that this news is sourced from https://libattery.ofweek.com/2025-08/ART-36001-8500-30668870.html and translated by SMM.